By Amy Castleton

Fonterra has announced its opening milk price for the 2021- 22 dairy season as a range of $7.25 – $8.75kgMS, with a midpoint of $8/kgMS. The $8 price is the highest on record for an opening price. In the 2013- 14 season where the co-operative paid a record $8.40/kg MS to farmers, Fonterra opened at $7/kg MS.

Chief executive Miles Hurrell commented that the improving global economic environment and strong demand for dairy, relative to supply, are sitting behind the strong forecast. He noted that global demand for dairy is continuing to grow, especially from China. At the same time, growth in global milk supply is muted, and the global supply of whole milk powder (WMP) is constrained.

However, there are a number of risks, including Covid-19, the impacts of governments winding back economic stimulus packages, foreign exchange volatility, changes in supply and demand patterns in the dairy market, and potential impacts of any geopolitical issues.

The NZX forecast for the 2021-22 season was $8.18/kgMS at the time of writing, well within Fonterra’s range, and higher than the midpoint.

At this point, this forecast is largely based on dairy commodity futures trading on the NZX Dairy Derivatives market, which continues to indicate relatively high commodity prices for the majority of the season; albeit with a downward trend to the forward curve for all four commodities. The Derivatives market does anticipate a larger drop in prices around September or October, as New Zealand heads into peak milk production.

The NZX forecast accounts for a NZ:US exchange rate of $0.721 US cents to the NZ dollar. The exchange rate has potential to swing over the next little while as the economic effects of the pandemic continue to be felt and most countries try to get back to something of normal life.

A one cent move in the exchange rate typically equates to a 10 cent move in the milk price.

Furthermore, we still have plenty of the season yet to run and we all know that plenty can change in the span of a season!

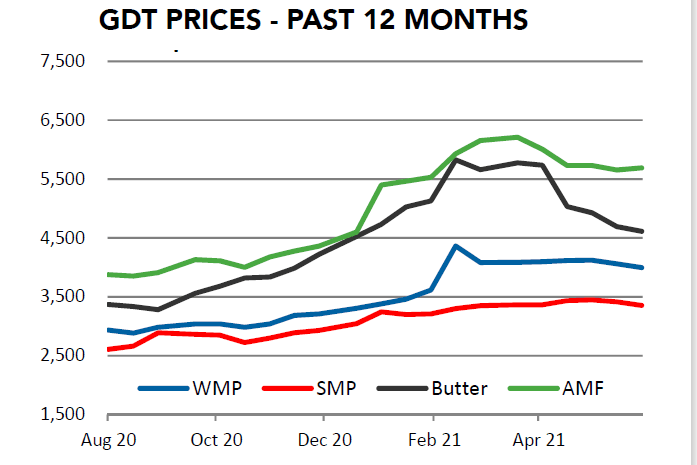

Global Dairy Trade (GDT) hasn’t put on much of a show for several events now, with the last six events seeing small moves in the price index. The last five GDT events have been down slightly. However prices remain at relatively high levels, particularly for milk powders. Butter and anhydrous milkfat are starting to be closer to historic averages than ‘high’ – prices for these commodities certainly aren’t low, though we have seen a downward push over recent months.

We did see a bit of a decrease in both WMP and skim milk powder at the June 15 GDT event, resulting in WMP prices dipping below US$4000/t on average. WMP has been priced over this level since the spike in March. The dip may see a bit more demand return to the market, outside of China, as more price sensitive regions will be more open to pay slightly lower prices. This should be supportive for relatively stable WMP prices.

Overall, the dairy market still feels stable, with supply and demand reasonably well balanced. We’re unlikely to see any significant drop in prices, instead it seems we will see a slow decline over coming months.

- Amy Castleton, senior dairy analyst at NZX Agri.